Navigating the Red-Mud Treatment Chemical Market (2026)

Why this matters:

Here's the reality – red mud (bauxite residue) represents one of the world's largest industrial waste problems. We're sitting on over 4 billion tonnes stockpiled globally, with another ~175 million tonnes added each year[1]. This material runs extremely alkaline (pH 10–12.5) and is loaded with iron, aluminum, silicon, titanium, calcium, and sodium oxides.

The bottom line? Procurement decisions in this space directly impact downstream costs, compliance outcomes, and environmental results. This article synthesizes findings from a 2026 market study to give procurement managers worldwide actionable intelligence they can actually use.

Understanding Red Mud's Composition and Challenges

The chemical makeup of red mud determines what treatment approaches will work. Typical oxide ranges vary significantly: Fe₂O₃ (5–60%), Al₂O₃ (5–30%), SiO₂ (3–50%), TiO₂ (0.3–15%), CaO (2–14%), and Na₂O (1–10%)[2].

The high alkalinity (pH 10–12.5) comes from residual sodium hydroxide carried over from the Bayer alumina extraction process. Here's what matters – particle morphology affects how it behaves. Bayer-process mud typically has fine-grained particles (2–18 µm) with high specific surface area, while sintering-process mud contains somewhat larger particles (1–20 µm) but maintains similar alkalinity[4].

What this means in practice: efficient neutralization isn't optional – it's essential. Research published in Toxics shows that red mud's alkalinity, combined with its iron/aluminum content, gives it strong capacity to adsorb heavy metals like cadmium[3]. Field trials found that adding just 5% red mud to acidic soil raised pH by 0.5 units and reduced cadmium bioavailability by 68%[5].

That's good news for soil remediation, but creates major challenges for industrial reuse. Neutralization with acids or CO₂, plus sodium control, becomes prerequisite just to meet environmental standards.

Figure 1 – A miniature diorama depicting key red mud composition parameters and pH characteristics. Tiny engineers emphasize the need for careful analysis when selecting treatment chemicals.

Market Reality Check: Sulfuric Acid and Ferrous Sulfate

Sulphuric acid (H₂SO₄)

Sulfuric acid remains the workhorse for lowering red mud pH and leaching metals. But here's the problem – its cost structure has undergone dramatic transformation.

Data from China's National Bureau of Statistics (via Zhiyan Consulting) tells a clear story: the average price of 98% industrial sulfuric acid in mid-January 2026 hit CNY 1,040.8 per tonne. That's a year-on-year increase of 127.5% – the highest January price point recorded in five years[6].

China remains the dominant global producer, but roughly half of its elemental sulfur feedstock comes from imports. This exposes buyers to international volatility and geopolitical supply risks that can't be ignored.

Ferrous sulphate (FeSO₄·7H₂O)

Ferrous sulfate plays three roles in red mud treatment: as a coagulant (removing suspended solids), as a reductant (converting toxic Cr(VI) to less harmful Cr(III)), and as a soil amendment (pH adjustment). It's produced mainly as a byproduct from sulfate-route titanium dioxide industry.

Since 2024, ferrous sulfate prices have climbed sharply – and there are three converging factors driving this: higher sulfuric acid input costs, anti-dumping duties on Chinese TiO₂ exports that constrain byproduct availability, and surging demand from lithium-iron-phosphate battery manufacturers competing for the same material.

Recent market monitoring shows just how dramatic this price escalation has been. On February 12, 2026, industrial-grade ferrous sulfate with ≥92% purity sold for CNY 680–800 per tonne in Henan province[7]. Lower-purity (~90%) material traded around CNY 480 per tonne, while 99% high-purity material showed wider price dispersion, ranging from CNY 230 to CNY 780 per tonne depending on supplier and regional market conditions.

Factory quotes compiled by ChemicalBook platform corroborate this range. On February 11, 2026, a Henan supplier offered ≥92% material at CNY 680/tonne, while a Hubei manufacturer priced 99% material at CNY 230/tonne[8].

Here's the context that matters – back in August 2025, comparable products sold for just CNY 180–350 per tonne[9]. In other words, prices have nearly doubled in six months.

Figure 2 – A miniature trading floor diorama highlighting dramatic price escalation. The price board shows that 98% sulfuric acid averaged 1,040.8 RMB/t in January 2026, while ferrous sulfate climbed from 180–350 RMB/t in August 2025 to 480–780 RMB/t by February 2026. The upward-trending graphs underscore persistent market tightness.

Alternative Neutralizing and Conditioning Agents

Given elevated acid prices and increasingly stringent environmental compliance requirements, operators are exploring a broader palette of treatment reagents:

Figure 3 – A miniature laboratory diorama showcasing alternative treatment reagents. Tiny scientists work with various chemicals including HCl, CO₂, gypsum, and oxalic acid, each serving distinct neutralization and conditioning roles.

Hydrochloric Acid (HCl) – proves valuable when pH only needs to drop to around 7.5. Its pricing tracks the chlor-alkali production cycle rather than sulfur markets, showing relative stability. However, procurement teams must ensure rigorous adherence to transport and storage regulations given HCl's corrosive properties and vapor hazards.

Carbon Dioxide (CO₂) – industrial CO₂ from flue-gas capture enables mild carbonation, typically lowering pH to around 10. This approach offers lower cost per unit of alkalinity neutralized compared to strong mineral acids, while potentially aligning with carbon-capture initiatives that generate carbon credits or regulatory compliance benefits.

Gypsum (CaSO₄·2H₂O) – widely available from flue-gas desulfurization systems. It acts as a finishing agent to reduce pH below 9 while supplying calcium for soil conditioning. Procurement specifications should emphasize low chloride content to avoid introducing secondary salinity issues in soil applications.

Specialized Reagents – oxalic acid, sodium hydroxide, and organic extractants serve niche roles in recovering rare earth elements and other valuable metals from red mud. These materials demand high purity grades, and their pricing responds to electronics and battery market dynamics rather than bulk chemical trends.

Selecting the Right Supplier

Our research framework employs a seven-dimensional supplier scorecard covering quality assurance, supply chain resilience, regulatory compliance, technical support capability, logistics efficiency, price transparency, and sustainability practices. Several critical insights emerge from this approach:

Figure 4 – A miniature boardroom scene depicting the supplier evaluation process. Tiny procurement managers review quality certificates, compliance documents, and the seven-dimension scorecard framework that guides strategic supplier selection.

Quality Must Lead – Require independent certificates of analysis for every batch, documenting not just primary component concentrations but also heavy-metal impurities and moisture content. Suppliers holding FAMI-QS certification or equivalent third-party quality system verification demonstrate process control and traceability necessary for consistent performance.

Supply Chain Resilience Creates Separation – Favor vendors who source feedstocks from multiple TiO₂ and sulfuric acid plants and maintain 30–60 day safety stocks strategically positioned at major ports. Transparent market intelligence and flexible packaging options signal operational maturity and customer-centric thinking.

Regulatory Compliance Grows More Complex Annually – Revised EU Industrial Emissions Directive (requiring member-state transposition by July 1, 2026) tightens discharge permit conditions and emphasizes waste minimization throughout the value chain. Ensure prospective vendors maintain complete REACH registrations and provide current GHS-compliant safety data sheets. Non-compliance risks cascade into your operations through supply interruptions and potential liability exposure.

Partnership > Transactional Efficiency – Select vendors who invest time understanding your specific red mud composition and can recommend optimized dosing rates and treatment sequences, rather than simply quoting commodity prices. Technical support capability becomes particularly valuable when processing campaigns encounter compositional variations or when exploring new valorization pathways.

Procurement Strategy That Works

Figure 5 – A miniature strategic planning office where tiny business strategists develop procurement frameworks. The scene illustrates key elements including 70/30 contract-spot balance, dual sourcing strategies, and total cost of ownership analysis.

Product Selection Should Match Treatment Objectives – Deploy industrial-grade H₂SO₄ or HCl for deep neutralization requirements (pH 12→9) and industrial CO₂ for moderate neutralization (pH 12→10). For leachate treatment and chromium reduction, FeSO₄ with ≥19% Fe content suffices. However, soil reclamation projects or any application that may enter the food chain demand feed-grade specifications (Pb <10 ppm, As <2 ppm), despite higher costs.

Contract Structure Should Balance Stability with Flexibility – Establish 12-month framework agreements with quarterly price review mechanisms. Commit approximately 70% of anticipated volume under contracted terms while preserving 30% capacity for spot market purchases. This approach captures favorable pricing opportunities during market dips while maintaining supply security. Implement dual sourcing for critical acids and salts across different geographic regions to mitigate localized supply disruptions.

Total Cost of Ownership Extends Well Beyond Unit Price – Freight typically represents 15–25% of TCO for bulk chemicals, while quality failures or compliance delays can add another 10–20% through production interruptions, rework, and expedited shipping. Investing in suppliers with robust quality management systems and proactive communication practices reduces these hidden costs more effectively than aggressive price negotiation on commodity specifications.

Looking Ahead

The red mud treatment chemical market will remain structurally tight throughout 2026. Official data confirms that 98% sulfuric acid prices in China hit a five-year high of CNY 1,040.8/t[6]. Ferrous sulfate prices have nearly doubled in six months[9], reflecting structural supply constraints and competition from battery materials.

Simultaneously, regulatory tightening in both the EU and China will continue pushing operators toward cleaner reagents and circular-economy solutions that transform waste streams into value-added products. Red mud's inherent characteristics – high pH and heavy-metal adsorption capacity[3] – also position it for potential applications in soil remediation and carbon-capture processes that could transform disposal costs into revenue streams.

For procurement professionals, the message is clear: understand the structural dynamics driving this market, build resilient supplier relationships, and plan for sustained cost pressure. The companies that navigate these challenges successfully won't just survive – they'll have competitive advantage.

Prepared by Uniwin Chemical, February 2026.

References

[1] Sun et al., 2025. *The Use of Red Mud in Agricultural Soil Cadmium Remediation: A Critical Review.* Toxics 14(1):16. This peer-reviewed paper discusses red mud composition and alkalinity, noting pH 10–12.5 and high Fe/Al contents[3], and reports that red mud amendments can raise soil pH and immobilize cadmium[5].

Available: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC12845953/

[2] Zhiyan Consulting via NBS, 2026. *Industrial Sulfuric Acid Price Monitoring.* Mid-January 2026 prices for 98% sulfuric acid reached CNY 1,040.8/t, up 127.5% year-on-year[6].

Available: https://www.zhiyan.com/reports/1251632.html

[3] China Report Hall & ChemicalBook, 2026. *Ferrous Sulfate Price Quotes.* February 2026 market data shows industrial-grade ferrous sulfate selling for 480–800 RMB/t, while August 2025 quotations were 180–350 RMB/t[7][8].

Related news

-

2024.11.15

Ferrous Sulfate: The Quiet MVP of Industrial Chemistry

Most procurement managers' view of ferrous sulfate reveals a cognitive blind spot: Cheap = unimportant. But here's the paradox: The same compound reduces toxic chromium in cement plants, catalyzes Fenton reactions in wastewater facilities, synthesizes hemoglobin in feed mills, and remediates heavy metals in soil. Four industries. Four technical requirements. One chemical purchased like a "commodity." The problem isn't ferrous sulfate. The problem is using a single dimension (price) to understand a multi-dimensional system (performance × context × risk). It's like using a bathroom scale to assess health—you get a number that tells you nothing. I didn't write this to "educate about ferrous sulfate." I wrote it to deconstruct: Why do we systematically underestimate "basic" things? Because complexity is hidden. Monohydrate vs. heptahydrate differences aren't on price lists. pH impact on reactions isn't in specs. Heavy metal gaps between feed-grade and industrial-grade aren't volunteered. What you don't know won't affect decisions—until it becomes a compliance audit, quality failure, or environmental fine. This article shows how to reframe "simple procurement" into "strategic choice." This isn't chemistry. This is about building high-resolution decision frameworks in information asymmetry. Real leverage hides in details "nobody cares about." -

2024.11.15

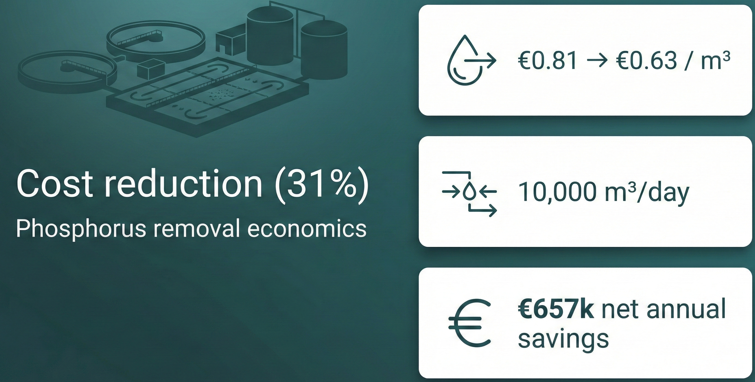

How a Polish Wastewater Plant Reduced Phosphorus-Removal Costs by 22%

Most operators lose the war on efficiency by winning the skirmish on procurement. They obsess over chemical invoices while ignoring the systemic entropy—corrosion—that devours their infrastructure from within. This technical case study of a Polish wastewater plant is more than just a report on switching chemicals; it is a cognitive reframe. It exposes a brutal reality: the "cheaper" input often demands a hidden, compounding tax in the form of corrosion, excessive maintenance, and accelerated capital depreciation. By shifting their lens from "invoice price" to "systemic health," this facility didn't just slash chemical costs by 31%. They broke free from the reactive maintenance spiral and reclaimed strategic mastery over their operational flow.